Fluid Liquidity Strategy

Basic Overview

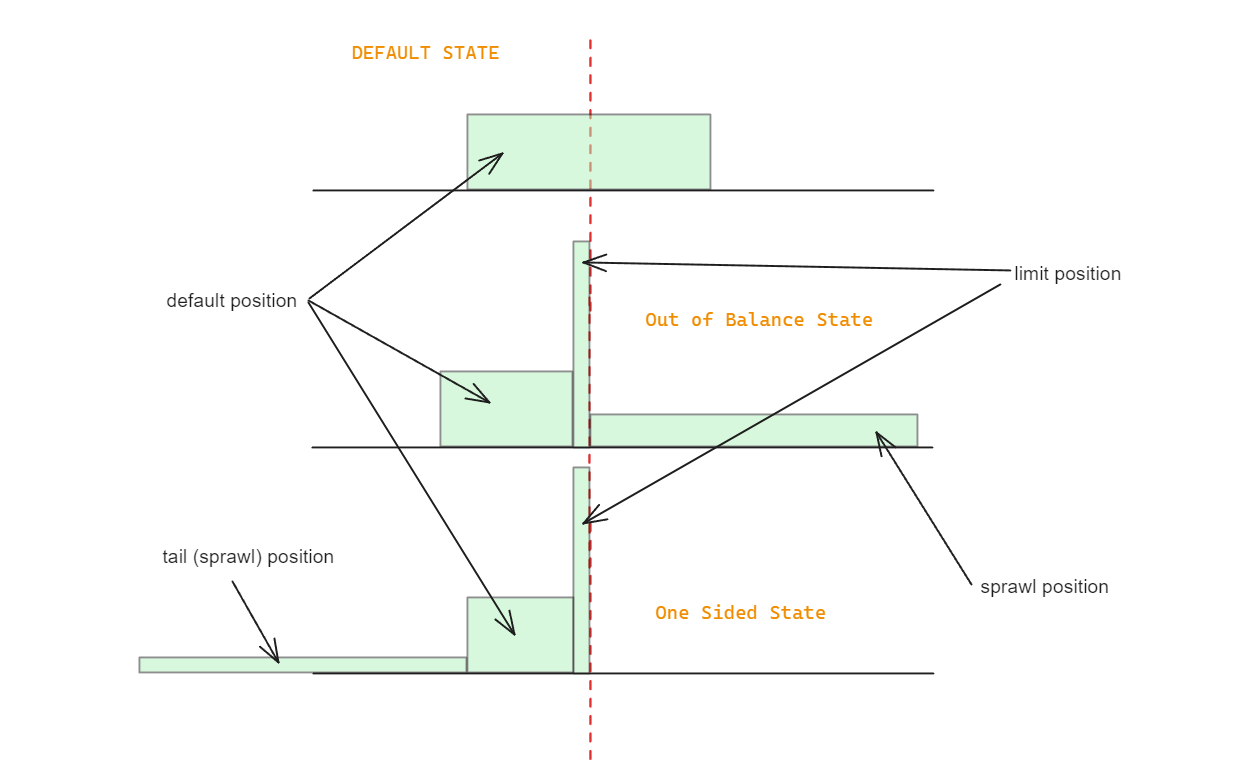

The Fluid Liquidity Strategy is an advanced, adaptable approach designed to optimize liquidity provisioning across a wide range of market conditions. It dynamically adjusts liquidity positions based on the current state of the asset ratio, offering three main states: default, unbalanced, and one-sided. This strategy excels in maintaining targeted asset ratios while efficiently distributing liquidity to capture trading fees and minimize impermanent loss.

Ideal Applications

This strategy also performs well in environments with low liquidity, markets where the vault holds the majority of funds, and is flexible in new chains and markets during maturity.

Advanced Description and Uses

Strategy Details

The Fluid Liquidity Strategy operates by:

- Dynamically managing states (default, unbalanced, one-sided) based on current asset ratios

- Maintaining a customizable ideal ratio between assets

- Adjusting position sizes based on the degree of imbalance from the ideal ratio

- Offering flexible sprawl position types for tailored liquidity distribution

- Enabling fine-tuning of liquidity allocation in one-sided scenarios

Key Features

- Dynamic State Management

- Customizable Ideal Ratio

- Flexible Sprawl Position Types

- Adaptive Position Sizing

- Tail Weight Configuration

Strategic Advantages

- Balanced Asset Management

- Optimized Fee Generation

- Impermanent Loss Mitigation

- High Customizability

Technical Explanation

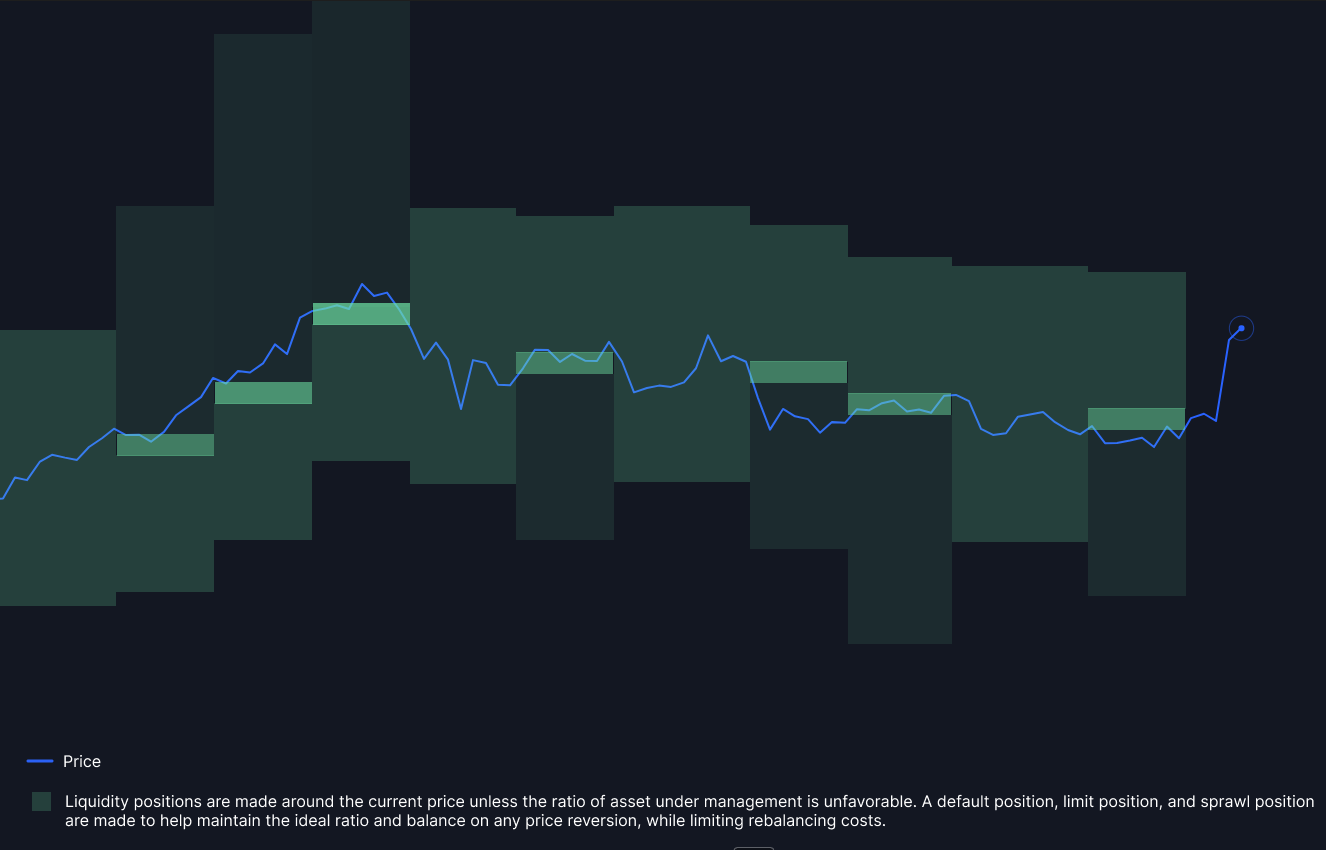

The Fluid Liquidity Strategy is designed to provide liquidity around the current price of a liquidity pool, with a focus on managing the asset ratio.

Core Mechanics

Position Types:

- Default Position: Single position around the current price when the vault has an acceptable asset ratio

- Limit Position: Uses surplus of oversupplied asset to catch price changes and reestablish ideal ratio

- Sprawl Position: Wide position to preserve majority of undersupplied asset while still actively market making

State Management:

- Transitions between default, unbalanced, and one-sided states based on current asset ratio

- Prioritizes asset ratio over ideal placement

- Does not use pool to exchange assets into a more favorable ratio

Parameter Configuration:

- Ideal Ratio: Specifies desired value ratio of token0 to token1 (based on value, not raw decimal amount)

- Acceptable Ratio Magnitude: Defines acceptable range for deviation from ideal ratio

- Position Size: Determines size of liquidity positions (measured in ticks)

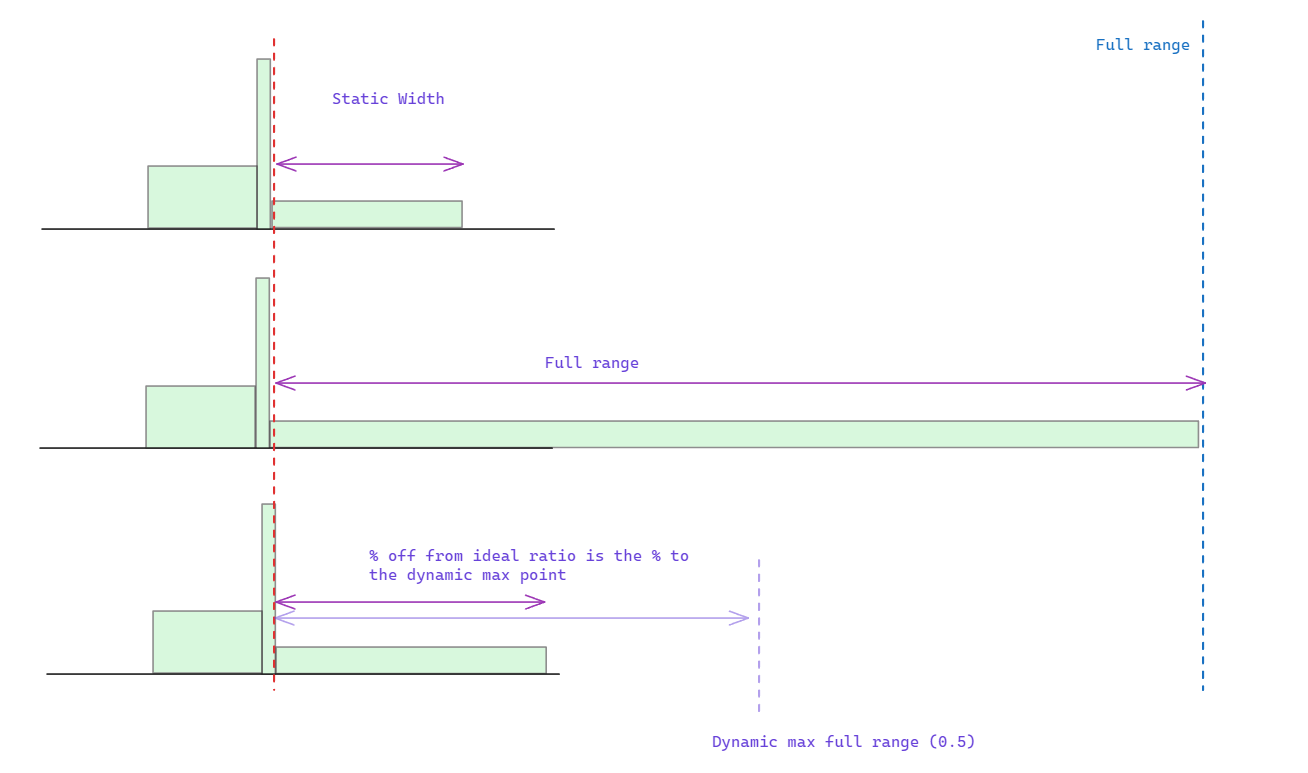

- Tail Sprawl Type: Determines range type for liquidity provision in unfavorable ratios

- Static Width: Number of ticks from current tick for sprawl position (for Static Range type)

- Tail Weight: Specifies percentage of weight allocated to long tail in one-sided scenarios

- Dynamic Max Full Range: Percentage of full range for maximum sprawl position size (for Dynamic Range type)

Sprawl Types:

- Full Range: Extends from current price to full range of pool

- Dynamic Range: Width determined by degree of imbalance from ideal ratio

- Static Range: Set width measured in ticks, extends from current tick

Detailed Parameter Explanation

Ideal Ratio:

- Example: For a 50:50 holding, set to 1

- For USD/ETH pair wanting 50:50, set to 1

Acceptable Ratio Magnitude:

- Example: For 10% deviation allowance, set to 1.1

- This allows ratio to be 55:50 to 45.45:50 before triggering unbalanced state

Position Size:

- Full size of position in ticks

- In non-default states, default position will be half or proportional of full range

- Can be aggressive if rebalancing frequently

- Consider using 1-day, 3-day, or 7-day average volatility

Static Width:

- Number of ticks from current tick for sprawl position

- Best for very stable pairs or medium volatility

Tail Weight:

- Maximum 0.5, default 0.1

- Set higher (e.g., 0.25) for infrequent rebalancing or highly volatile tokens

Dynamic Max Full Range:

- Percentage of full range for maximum sprawl position size

- Actual width based on deviation from ideal ratio

Implementation Considerations

- Gas Usage: High frequency of position adjustments may lead to significant gas consumption

- Rebalancing Frequency: Should be set based on historical volatility and desired responsiveness

- Parameter Tuning: Requires careful consideration of asset characteristics, market conditions, and risk tolerance

- Best Used For:

- Pairs with medium to high volatility when optimizing total return

- Pools with limited liquidity

- Scenarios where the vault will hold the majority of the pool's liquidity

Deciding Parameters

Default Position Size:

- Aim for smallest possible size that won't go out of range between execution intervals

- Example: For 4-hour execution interval, consider 3-month historical 4h candles

- Being overly narrow is less problematic due to reduced rebalancing fees

Acceptable Change Parameter:

- Default of 1.1 is suitable for most cases

Sprawl Type Selection:

- Low static for stables and LST with natives (e.g., 10% for wstETH/ETH pool)

- Larger static width for medium assets (e.g., 70% for BTC/USD)

- Dynamic for general use, full range when in doubt

- For dynamic, use lower values (e.g., 0.05) with high counter liquidity, higher values (e.g., 0.5) for more volatile tokens

By offering this level of dynamic asset management and customization, the Fluid Liquidity Strategy enables liquidity providers to create sophisticated approaches that can effectively maintain desired asset ratios, optimize fee generation, and adapt to various market conditions while mitigating impermanent loss risks.